Free SIP Calculator (Systematic Investment Plan)

See how consistent monthly investing builds long-term wealth

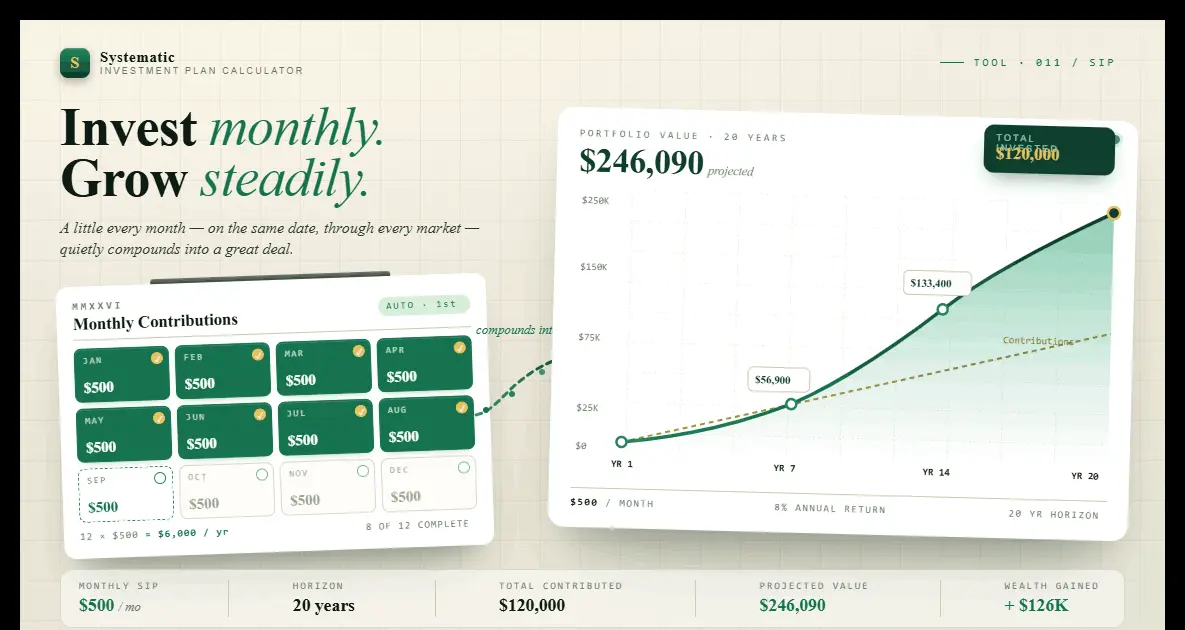

Your SIP plan

Free · No sign-up · Updates as you typeUS$

Amount you invest each month, for example 500.

Optional. Picks an approximate long-run rate by asset mix. Edit the field below for your own.

Expected annual growth rate, for example 7 for 7%. A long-run global equity average is roughly 7% to 10% before inflation.

How many years you plan to keep investing, from 1 to 50.

Optional refinements

Raise your monthly amount by this much each year. Leave at 0 for a flat SIP.

Optional. Set this to see your corpus in today's money. Leave at 0 to ignore inflation.

Final Value (Your Corpus)

US$ 261,983

In plain terms: you invest US$ 500 a month for 20 years. That is US$ 120,000 of your own money. Growing at 7% a year, compounding turns it into US$ 261,983, of which US$ 141,983 is growth you never paid in.

Your money vs the growth on top

Total Invested

US$ 120,000

Estimated Returns

US$ 141,983

Returns on Investment

118.3%

Portfolio Growth Over Time

Year-by-Year Breakdown

| Year | Invested | Returns | Total Value |

|---|---|---|---|

| 1 | US$ 6,000 | US$ 232 | US$ 6,232 |

| 2 | US$ 12,000 | US$ 915 | US$ 12,915 |

| 3 | US$ 18,000 | US$ 2,082 | US$ 20,082 |

| 4 | US$ 24,000 | US$ 3,766 | US$ 27,766 |

| 5 | US$ 30,000 | US$ 6,005 | US$ 36,005 |

| ... | |||

| 16 | US$ 96,000 | US$ 81,162 | US$ 177,162 |

| 17 | US$ 102,000 | US$ 94,201 | US$ 196,201 |

| 18 | US$ 108,000 | US$ 108,617 | US$ 216,617 |

| 19 | US$ 114,000 | US$ 124,508 | US$ 238,508 |

| 20 | US$ 120,000 | US$ 141,983 | US$ 261,983 |

Insight: Notice how returns accelerate in the later years. That is compounding at work. The earlier you start your SIP, the more time your returns have to generate further returns.

How your corpus moves: return rate vs years invested

A SIP result swings most on two things you do not fully control: the return you actually earn and how long you stay invested. This grid recomputes your final corpus across a range of both, keeping your monthly amount and step-up fixed. Your current pick is highlighted, so you can see the trade-off without retyping anything.

| Return ↓ / Years → | 10y | 15y | 20y | 25y | 30y |

|---|---|---|---|---|---|

| 4% | US$ 73,870 | US$ 123,455 | US$ 183,999 | US$ 257,922 | US$ 348,181 |

| 5.5% | US$ 80,119 | US$ 140,012 | US$ 218,812 | US$ 322,490 | US$ 458,900 |

| 7% | US$ 87,047 | US$ 159,406 | US$ 261,983 | US$ 407,399 | US$ 613,544 |

| 8.5% | US$ 94,736 | US$ 182,175 | US$ 315,720 | US$ 519,684 | US$ 831,199 |

| 10% | US$ 103,276 | US$ 208,962 | US$ 382,848 | US$ 668,945 | US$ 1,139,663 |

A Systematic Investment Plan (SIP) is a strategy of investing a fixed amount at regular intervals, typically monthly. This calculator uses the future value of an annuity-due formula, which assumes each payment is made at the beginning of the period and immediately starts compounding:

FV = PMT × [((1 + r)^n − 1) / r] × (1 + r)

Where PMT = monthly investment, r = monthly rate (annual rate ÷ 12), and n = total months. When you set an annual step-up, the calculator raises PMT each year and sums the result month by month.

Step 1: Pick your currency and enter the amount you plan to invest each month.

Step 2: Set an expected annual return. For global equity index funds, 7% to 10% is a common historical range. Use 5% to 6% for a more conservative estimate.

Step 3: Choose your duration in years. Longer periods raise the final corpus sharply, thanks to compounding.

Step 4: Optionally add an annual step-up or an inflation rate. The corpus, breakdown, growth chart, table, and sensitivity grid all update as you type. No button to press.

What Is a Systematic Investment Plan (SIP) and How Does Compounding Work?

A Systematic Investment Plan is a disciplined approach to building wealth: you invest a fixed amount at regular intervals, usually monthly, regardless of market conditions. Rather than trying to time the market, SIP investing uses time in the market as its primary advantage. Each monthly contribution starts compounding immediately, and the returns on earlier contributions generate their own returns in later years. That creates an accelerating wealth curve that lump-sum investors often underestimate.

SIP returns compound in a way that turns even modest monthly amounts into significant wealth. A monthly SIP of 500 at 7% annual return for 20 years grows to roughly 262,000, on total contributions of just 120,000. The remaining 142,000 or so is pure compounding. One nuance is worth understanding: the sequence of returns matters. Early strong returns in a SIP have a smaller impact than you might expect, because you have little invested yet. Late strong returns matter more. Our sequence-of-returns calculator explores this in depth, an essential complement to any SIP projection.

Why a Step-up SIP Beats a Flat One

A flat SIP keeps the same monthly amount for decades, but your income rarely stays flat. A step-up SIP raises the contribution by a set percentage every year, often to match a pay rise, so your investing grows with your earning power. The effect is larger than most people expect. Because each annual increase is invested for all the remaining years, a 5% yearly step-up on a 20-year plan can lift the final corpus well above a flat SIP at the same starting amount. The optional step-up field above lets you test this directly: set it to your expected raise and watch the corpus and the year-by-year table respond.

SIP Investing as a Foundation for Building Net Worth

SIP investing is one of the most reliable foundations for growing net worth over time. Consistent monthly contributions remove the behavioural risk of trying to invest "at the right time," and the automatic nature of a SIP creates a forced saving habit that builds wealth almost invisibly. Worthmap is a global net worth calculator and investment tracker where you can follow your actual portfolio alongside SIP projections. Seeing the gap between your real holdings and your target corpus is one of the most motivating signals an investor can have.

Once you have established SIP discipline, the natural next step is portfolio rebalancing: keeping your asset allocation aligned with your target mix as different asset classes grow at different rates. Our portfolio rebalancing calculator shows exactly what to buy and sell to realign your portfolio, a step that most SIP investors skip.

Tracking SIP Progress Across Currencies with Worthmap

For expats and digital nomads managing money across borders, running a SIP in one currency while living in another adds a layer of FX complexity that most calculators ignore. Worthmap works as a multi-currency investment tracker that consolidates your SIP investments, whether in USD index funds, EUR bonds, or SGD equities, into a single net worth view with real-time conversion. That gives you a realistic picture of your SIP progress regardless of which market you invest in or which currency you currently earn in.

As a global finance app and online asset tracker, Worthmap is built for investors who operate across multiple currencies and jurisdictions. The SIP calculator above supports many currencies because SIP investing is not just an India-specific idea. It is the global name for systematic, disciplined, recurring investing, practised by expats and long-term investors worldwide.

SIP Investing vs Budgeting Apps: Why Globally Mobile Investors Need More

Many investors start with a budgeting app. But traditional budgeting tools, including many YNAB alternatives, are built around single-currency household finances. They track cash flow well, yet they struggle with multi-currency portfolios, international brokerage accounts, and cross-border investments. Plenty of people come to Worthmap specifically looking for a YNAB alternative that handles international accounts and multiple currencies. For globally mobile investors running a SIP across different markets, Worthmap is a better fit: it is built for investment tracking, not just budgeting, and it handles the FX complexity that makes standard tools fall short.

Linking SIP Consistency to Financial Independence Goals

Staying consistent with a SIP is easier when you have a clear target to work toward. Without a financial independence number, it is tempting to treat a SIP as abstract, just figures growing somewhere. Worthmap's barista FIRE calculator helps you work out what your target corpus actually needs to be, linking SIP discipline to a concrete goal. Once you know your number, every monthly contribution becomes a measurable step toward a specific milestone rather than a vague saving habit.

Frequently Asked Questions About the SIP Calculator

A SIP calculator projects the future value of regular monthly investments by applying compound interest. You enter your monthly investment amount, expected annual return rate, and investment duration. The calculator applies the future value of an annuity-due formula, FV = PMT × [((1 + r)^n − 1) / r] × (1 + r), where r is the monthly rate and n is the total number of months. The result shows your total corpus, total invested, and the estimated returns generated by compounding.

A step-up SIP raises your monthly contribution by a fixed percentage every year, usually in line with your salary growth. Because each annual increase is then invested for the rest of the term, a modest step-up can lift the final corpus substantially. The optional step-up field in this calculator lets you compare a flat SIP against one that grows over time, without doing the maths by hand. Set the step-up to your expected annual pay rise to get a realistic projection.

It can. The headline corpus is a nominal figure, the actual currency amount you would hold at the end. Inflation quietly reduces what that amount can buy, so this tool includes an optional inflation field. Enter an expected average inflation rate and the calculator also shows the inflation-adjusted, or real, value in today's purchasing power. Comparing the two numbers is a useful reality check, because a large nominal corpus decades from now buys less than the same figure does today.

Lump-sum investing deploys all available capital at once, maximising time in the market from day one. SIP investing spreads capital over time in regular instalments. Research consistently shows lump-sum investing outperforms SIP in roughly two-thirds of historical market scenarios, because more capital is exposed to compound growth sooner. SIP still excels in behavioural terms: it removes the pressure of timing the market, is easier to maintain consistently, and is the only realistic approach for investors building capital incrementally from earned income rather than deploying a windfall.

Yes. Worthmap consolidates investment accounts, brokerage holdings, and assets across multiple currencies into a single net worth dashboard with real-time FX conversion. If you have a SIP running in USD index funds, a separate EUR bond portfolio, and equity holdings in SGD, Worthmap aggregates all of them and shows your total net worth in whichever base currency you choose. This matters for expats and digital nomads whose SIP may be denominated in a different currency from their income or expenses.

A SIP builds your portfolio steadily over time, but different asset classes grow at different rates, so your allocation drifts away from your target mix. If you started with a 70/30 equity to bond split and equities have outperformed, your portfolio may now sit at 80/20 or higher. Rebalancing restores your target allocation, which has two benefits: it enforces a systematic "buy low, sell high" discipline (you trim what has grown and add to what has lagged), and it manages risk by stopping any single asset class from dominating. Annual or semi-annual rebalancing is the typical approach for SIP investors.

Track Your Real SIP Progress with Worthmap

Projections are the starting point. Worthmap is the online asset tracker and investment monitoring app built for expats and digital nomads, consolidating your SIP portfolio, international accounts, and multi-currency holdings into one real-time net worth dashboard.

Sign Up for Worthmap