Graham Number Calculator

Benjamin Graham's formula for intrinsic value

Enter your stock details

Free · No sign-up · Updates as you type$

Net profit per share, e.g. 4.50. Use the last 12 months.

$

Net worth per share. No figure? Use the helper below.

$

Add the market price to see cheap vs expensive.

Intrinsic Value (Graham Number)

$51.06

per share

0.67x

33%

In plain terms: on Graham's conservative yardstick, this stock is worth up to about $51.06 per share, from earnings of $4.50 and book value of $25.75. At $34.00, that is 0.67x the Graham Number, a discount of about 33% to intrinsic value.

EPS Used

$4.50

Book Value Used

$25.75

What This Means: Stock is trading below its intrinsic value with a good margin of safety. Consider this undervalued and potentially attractive for value investors.

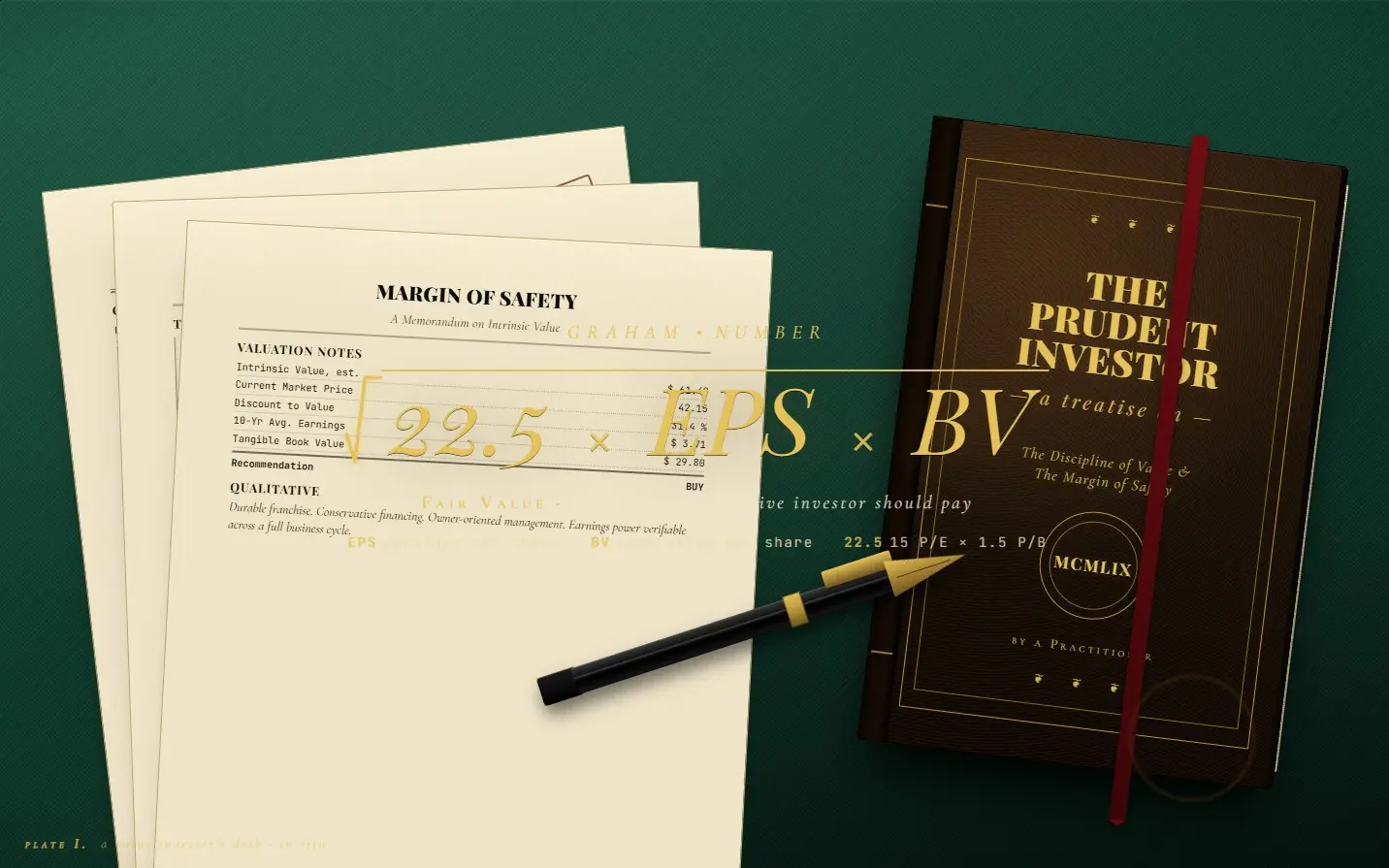

The Graham Number is a formula developed by Benjamin Graham, widely considered the father of value investing and mentor to Warren Buffett. It provides a conservative estimate of a stock's intrinsic value.

Graham Number = √(22.5 × EPS × Book Value per Share)

Where:

Graham believed investors should only buy stocks when the current price is no more than 50% of the Graham Number, providing a significant margin of safety.

Step 1: Find the company's EPS (Earnings Per Share) - usually available on financial websites or in quarterly reports.

Step 2: Find the Book Value Per Share - calculated as (Total Assets - Total Liabilities) ÷ Number of Shares Outstanding.

Step 3: Enter both values and the Graham Number appears instantly, no button to press.

Step 4: Compare the Graham Number with the current stock price to assess if the stock is potentially undervalued.

What Is the Graham Number?

The Graham Number is a stock valuation metric created by Benjamin Graham, widely regarded as the father of value investing and the mentor of Warren Buffett. It provides a quick estimate of the maximum price a defensive investor should pay for a stock, based on two fundamental measures: earnings per share (EPS) and book value per share (BVPS).

If a stock's current market price is below its Graham Number, it may be undervalued according to Graham's conservative framework. If the price is above the Graham Number, the stock may be overpriced relative to its fundamental earnings and asset base.

The Graham Number Formula

Graham Number = √(22.5 × EPS × BVPS)

The constant 22.5 is the product of Graham's two maximum acceptable ratios: a P/E ratio of 15 multiplied by a P/B ratio of 1.5 (15 × 1.5 = 22.5). This means the formula is essentially calculating the price at which a stock would simultaneously trade at a P/E of 15 and a P/B of 1.5 — Graham's upper bounds for a conservatively valued stock.

If either EPS or BVPS is negative, the formula cannot produce a meaningful result. The Graham Number is only applicable to companies with positive earnings and positive book value, which means it works best for established, profitable businesses with tangible assets.

How to Calculate the Graham Number Step by Step

First, find the company's earnings per share. This is the net income divided by the total number of outstanding shares. Use the trailing twelve-month (TTM) figure for the most current picture. Graham himself recommended using an average of the past three years of earnings to smooth out temporary fluctuations.

Second, find the book value per share. This is total shareholders' equity divided by the total number of outstanding shares. You can find this on the company's balance sheet. Some analysts prefer using tangible book value, which excludes goodwill and intangible assets, for a more conservative estimate.

Enter both values into the calculator and it will compute the Graham Number instantly. Compare the result to the stock's current market price to see whether it appears undervalued or overvalued by Graham's standards.

Interpreting the Results

When the current stock price is below the Graham Number, it suggests the stock may be trading at a discount to its intrinsic value — a potential buying opportunity for value investors. The larger the gap between the stock price and the Graham Number, the greater the implied margin of safety.

The Price-to-Graham-Number ratio provides a quick summary. A ratio below 1.0 suggests potential undervaluation. A ratio of 1.0 indicates fair value by Graham's criteria. A ratio above 1.0 suggests the stock is priced above what Graham would consider conservative value.

Limitations of the Graham Number

It does not account for future growth. Companies with strong earnings growth prospects — particularly technology and software firms — will almost always appear overvalued by the Graham Number because it only looks at current earnings and book value.

It only works for profitable companies with positive book value. Businesses that are pre-revenue, loss-making, or asset-light (such as many SaaS companies) will produce meaningless results.

Finally, the Graham Number should never be used in isolation. Graham himself embedded it within a broader framework of criteria for defensive stock selection, including requirements for dividend history, earnings consistency, and adequate company size. The number is a starting point for research, not a final verdict.

Graham Number vs Other Valuation Methods

The Graham Number sits alongside several other valuation approaches. The Discounted Cash Flow (DCF) model projects future free cash flows and discounts them back to present value, making it more comprehensive but requiring assumptions about growth and discount rates. The PEG ratio adjusts the P/E ratio for expected earnings growth, making it more suitable for growth stocks. For value investors following Benjamin Graham's philosophy, the Graham Number provides the fastest and most objective initial screen — it requires no subjective assumptions about the future, only hard numbers from the financial statements.

Frequently Asked Questions

Both figures are available on financial data websites such as Yahoo Finance, Google Finance, Morningstar, or your brokerage platform. Look for "Earnings Per Share (TTM)" and "Book Value Per Share" in the company's fundamental data section.

Diluted EPS is the more conservative choice, as it accounts for stock options, convertible securities, and other potential dilution. Graham favoured conservative figures, so diluted EPS aligns with his philosophy.

Yes. The formula works for any stock on any exchange, in any currency. The intrinsic value will be expressed in the same currency as the EPS and BVPS inputs.

A Price-to-Graham-Number below 0.75 suggests a meaningful discount and a strong margin of safety. Between 0.75 and 1.0 is still potentially attractive. Above 1.0 suggests the stock exceeds Graham's conservative valuation criteria.

Absolutely — and Graham recommended it. Using the average of the last 3 years of EPS gives a more stable result, especially for cyclical industries like mining, energy, or banking where single-year earnings can swing significantly.

Dividend Yield, Dividend Growth & the PEG Ratio for Value Investors

Value investors who follow Benjamin Graham's approach often combine the Graham Number with dividend analysis. Dividend yield — annual dividends per share divided by the stock price — rewards patient investors while they wait for a stock to reach its intrinsic value. A stock trading below its Graham Number that also pays a dividend yield above 3% offers a "paid to wait" scenario: you collect income while the market eventually re-rates the stock to fair value. Dividend growth calculator tools project how that income stream grows over time as companies raise their dividends annually.

Dividend growth investing focuses on companies that consistently increase their dividends — the "Dividend Aristocrats" (25+ years of consecutive increases) and "Dividend Kings" (50+ years). These companies tend to have durable competitive advantages and predictable earnings — the same characteristics Graham valued. A dividend discount model calculator values these stocks by discounting all future dividend payments back to present value. The Gordon Growth Model simplifies this: P = D₁ / (r − g), where a higher dividend growth rate increases the stock's intrinsic value.

The PEG ratio (Price/Earnings to Growth) adjusts the P/E ratio for expected earnings growth, making it more relevant for growth stocks than the pure Graham Number. PEG = (P/E Ratio) / Annual EPS Growth Rate. A PEG below 1.0 is generally considered undervalued; above 2.0 suggests premium pricing relative to growth. While Graham preferred static earnings power over growth projections, modern value investors use the PEG ratio to extend Graham's framework to faster-growing businesses. Combined with the Graham Number as a floor valuation and the PEG ratio as a growth-adjusted ceiling, value investors can bracket the fair value of almost any profitable company.

Screen Stocks Like a Value Investor

The Graham Number is just the beginning. Worthmap helps you apply Benjamin Graham's full framework — including earnings consistency, dividend history, and margin of safety — to find genuinely undervalued stocks across global markets.

Explore Worthmap