WACC Calculator

Weighted Average Cost of Capital for any company

Enter Capital Structure Data

Capital Structure

$

Share price × shares outstanding: the company's market capitalisation (E).

$

All interest-bearing debt: short- and long-term borrowings (D).

Cost Rates

Return shareholders expect (Re). Don't know it? Use the CAPM helper below.

Average interest rate on the company's debt, before tax (Rd).

Optional: picks an approximate statutory rate. Edit the field below for your exact rate.

Effective corporate tax rate: makes interest tax-deductible (e.g., 21).

WACC Calculator Results

Weighted Average Cost of Capital (WACC)

7.56%

Capital Structure

Equity Weight

71.4%

Debt Weight

28.6%

Equity Contribution

6.43%

Debt Contribution

1.13%

After-Tax Cost of Debt

3.95%

Insight: A company's WACC represents the minimum return it must earn on existing assets to satisfy its creditors, owners, and other capital providers. Projects with returns above the WACC create value; those below destroy it.

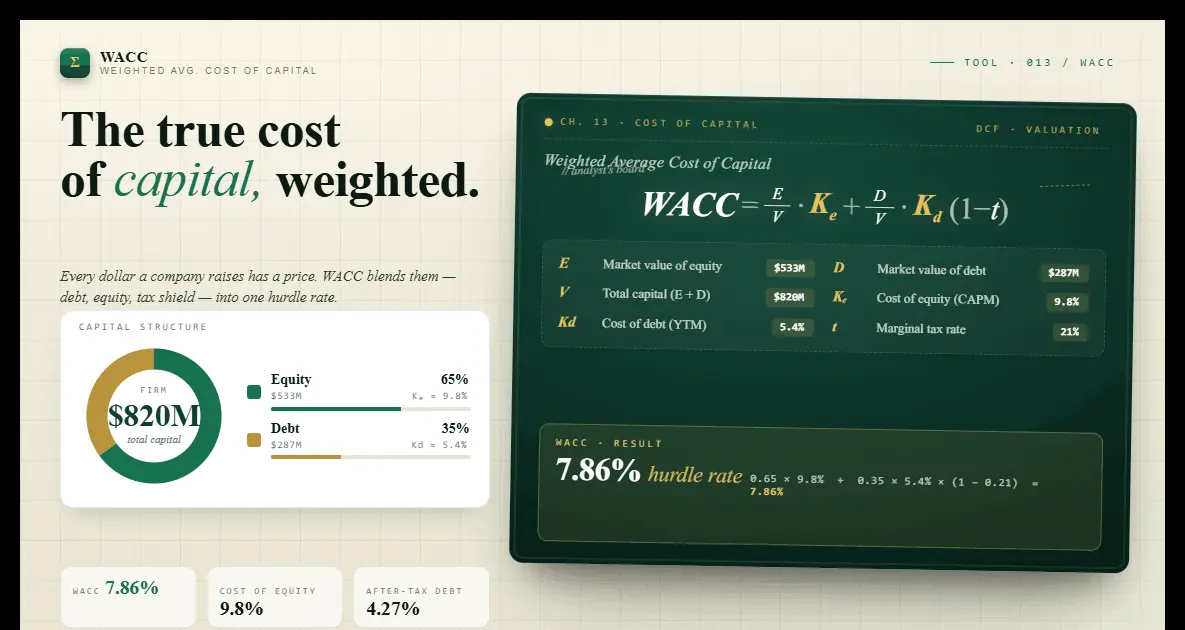

The Weighted Average Cost of Capital (WACC) is the average rate a company is expected to pay to finance its assets. It blends the cost of equity and the after-tax cost of debt, weighted by their respective proportions in the capital structure.

WACC = (E/V × Re) + (D/V × Rd × (1 − T))

Step 1: Enter the market value of equity (market cap) and market value of debt (total outstanding debt).

Step 2: Enter the cost of equity (often estimated using CAPM: Risk-Free Rate + Beta × Market Risk Premium).

Step 3: Enter the cost of debt (average interest rate on borrowings) and the corporate tax rate.

Step 4: Click Calculate to see the WACC, capital weights, and contribution breakdown.

What Is WACC (Weighted Average Cost of Capital)?

The Weighted Average Cost of Capital (WACC) is one of the most important metrics in corporate finance. It represents the blended cost a company pays to finance its operations through a mix of equity and debt. WACC is the minimum rate of return a company must earn on its existing asset base to satisfy its investors, creditors, and other capital providers.

WACC is heavily used in discounted cash flow (DCF) analysis as the discount rate applied to future free cash flows. A higher WACC means future cash flows are worth less today, resulting in a lower company valuation.

The WACC Formula Explained

WACC = (E/V × Re) + (D/V × Rd × (1 − T))

The formula weights each source of capital by its proportion in the total capital structure. The cost of debt is adjusted for the tax shield because interest payments are tax-deductible.

The cost of equity is typically estimated using the Capital Asset Pricing Model (CAPM): Re = Risk-Free Rate + Beta × Equity Risk Premium.

How Is WACC Used in Practice?

Investment analysts use WACC as the discount rate in DCF models to value companies and stocks. If a company's return on invested capital (ROIC) exceeds its WACC, it is creating economic value.

Corporate managers use WACC as a hurdle rate for capital budgeting decisions. Any new project must generate returns above the WACC to be considered value-creating.

Limitations of WACC

WACC assumes a constant capital structure. In reality, a company's mix of debt and equity changes over time.

WACC is most reliable for established companies with stable capital structures. For startups or high-growth companies, WACC may not accurately reflect the true cost of capital.

Frequently Asked Questions About the WACC Calculator

There is no universal good WACC. It varies by industry. Most established companies have a WACC between 6% and 12%.

The cost of equity is estimated using CAPM: Cost of Equity = Risk-Free Rate + Beta × Market Risk Premium. Beta can be found on financial data sites.

Interest payments on debt are tax-deductible, which reduces the effective cost of borrowing. This tax shield makes debt financing cheaper than equity.

CAPM Calculator: Estimating Beta and the Cost of Equity

The Capital Asset Pricing Model (CAPM) is the standard method for estimating the cost of equity in the WACC formula. The CAPM formula is: Re = Rf + β × (Rm − Rf), where Rf is the risk-free rate (typically the 10-year government bond yield), β (beta) is the stock's systematic risk relative to the market, and (Rm − Rf) is the equity risk premium. Beta below 1 means the stock moves less than the market; beta above 1 means it amplifies market moves. A beta calculator helps you estimate this input from historical price data.

In practice, analysts use industry beta (also called unlevered or asset beta) as a starting point, then re-lever it for the company's specific debt-to-equity ratio. This prevents the cost of equity estimate from being distorted by the company's capital structure. Re-levering uses the Hamada equation: βL = βU × [1 + (1 − T) × (D/E)], where T is the tax rate and D/E is the debt-to-equity ratio. This is why the same WACC calculator is used both as a CAPM calculator (to get Re) and as a capital structure optimisation tool.

Enterprise Value Calculator, EBITDA & Valuation Multiples

Enterprise value (EV) is the total value of a business — the theoretical takeover price. EV = Market Capitalisation + Total Debt − Cash and Cash Equivalents. Unlike market cap, EV accounts for a company's debt load, making it a more complete measure of what you are actually paying when you acquire a business. An enterprise value calculator is essential for comparing companies with different capital structures — a company with high debt and low market cap may be worth less than its market cap suggests.

EBITDA — Earnings Before Interest, Taxes, Depreciation and Amortisation — is the most common denominator in relative valuation. The EV/EBITDA multiple (enterprise value divided by EBITDA) is used to compare companies across industries because it is capital-structure neutral and removes the effects of differing tax rates and accounting depreciation choices. An EBITDA calculator starts with operating income (EBIT) and adds back depreciation and amortisation. WACC is the bridge between EBITDA-based multiples and DCF analysis: in a DCF model, WACC discounts free cash flows (which are derived from EBITDA less capex, taxes, and working capital changes) back to their present value.

Take Your Financial Analysis Further

WACC is a building block of professional valuation. Combine it with portfolio tracking, multi-currency net worth monitoring, and AI-powered insights on Worthmap.

Sign Up for Worthmap